Quick Answer

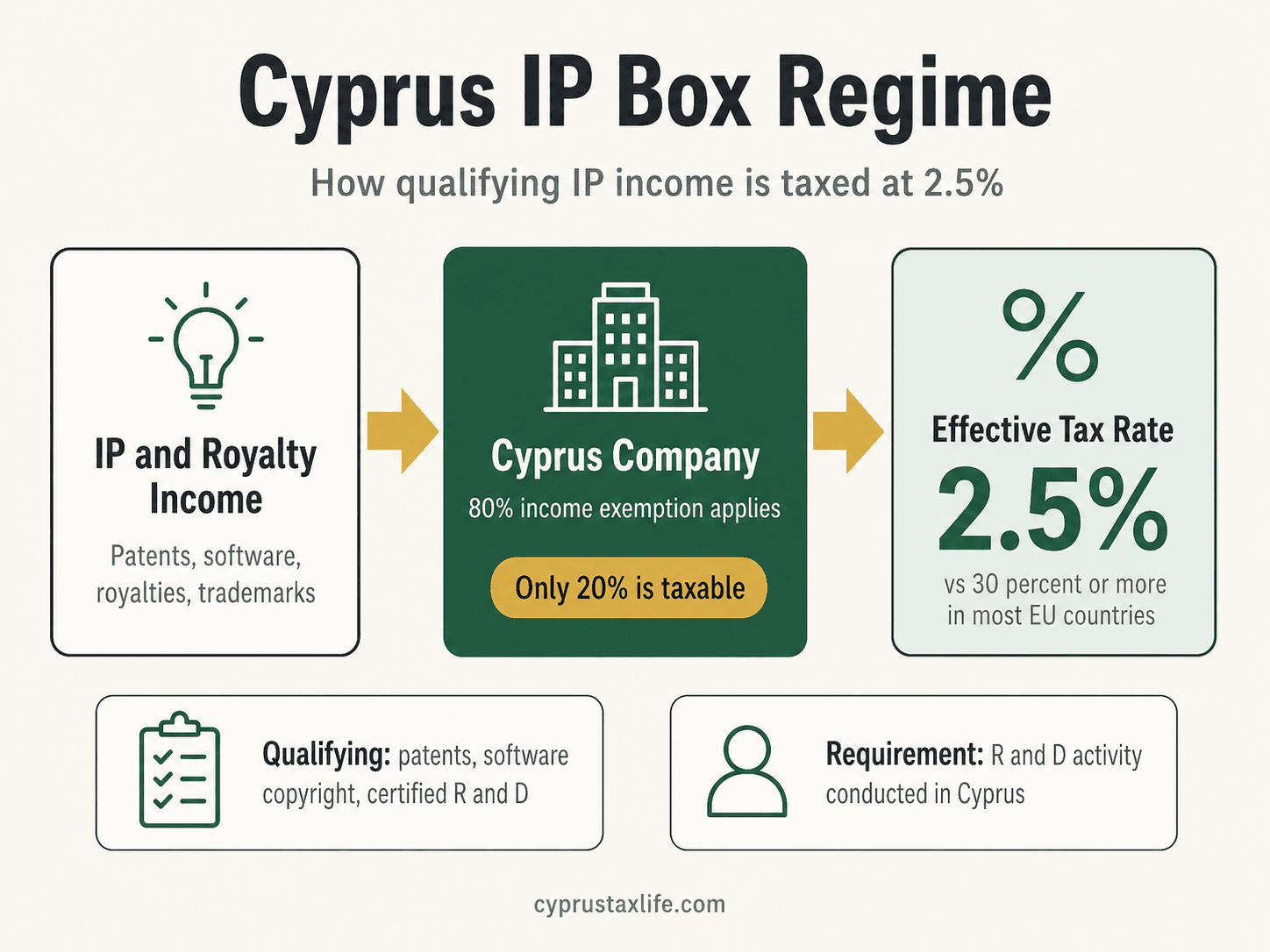

The Cyprus IP Box regime taxes qualifying intellectual property income at an effective rate of approximately 2.5% corporate tax. An 80% deduction applies to net profit from qualifying IP assets including patents, software, and know-how developed by the company. The regime is OECD-compliant under the modified nexus approach and has no sunset clause.

Key Facts 2026

| Effective tax rate on qualifying IP income | ~2.5% |

| Exemption on qualifying net profit | 80% |

| Corporate tax on remaining 20% | 15% |

| Qualifying assets | Patents, software copyright, plant variety rights, similar IP |

| Non-qualifying (excluded) | Trademarks, brands, marketing intangibles, know-how |

| OECD nexus requirement | R&D expenditure must be by the qualifying company |

| Effective rate vs EU competitors | Cyprus 2.5% vs Netherlands 9% vs Luxembourg 6.8% |

| Combined with Non-Dom | Dividends still at 2.65% GHS only |

Cyprus IP Box: 2.5% Tax on Intellectual Property Income

Cyprus's IP Box regime offers an 80% exemption on qualifying income from intellectual property, reducing the effective corporate tax rate to just 2.5%. One of the most competitive IP regimes in the EU.

Last updated:

Cyprus IP Box: NEXUS Ratio - Worked Example (3 Scenarios)

The NEXUS approach limits the IP Box benefit to income proportional to genuine R&D activity. Outsourcing development to related parties reduces the benefit significantly.

| Variable | A - All R&D in-house | B - Mixed (50% in-house) | C - Mostly outsourced |

|---|---|---|---|

| Qualifying IP income | €500,000 | €500,000 | €500,000 |

| Qualifying R&D costs (in-house / unrelated) | €200,000 | €100,000 | €20,000 |

| Total R&D costs (incl. related-party outsourcing) | €200,000 | €200,000 | €200,000 |

| NEXUS ratio | 100% (200/200) | 50% (100/200) | 10% (20/200) |

| Qualifying profit (income x 80% exemption) | €400,000 | €400,000 | €400,000 |

| Exempt profit (qualifying x NEXUS) | €400,000 | €200,000 | €40,000 |

| Taxable profit remaining | €100,000 | €300,000 | €460,000 |

| Corporation tax at 15% | €15,000 (3% effective) | €45,000 (9% effective) | €69,000 (13.8% effective) |

Takeaway: The 2.5% effective rate (Scenario A) requires all R&D to be performed by the Cyprus company itself or contracted to unrelated third parties. Related-party outsourcing (e.g. to a parent company) does not qualify for the enhanced NEXUS ratio and will push the effective rate toward 15%.

Frequently Asked Questions

What is the effective tax rate under the Cyprus IP Box?

Does software qualify for the Cyprus IP Box?

Is the Cyprus IP Box OECD compliant?

Do trademarks and brands qualify for the Cyprus IP Box?

What is the nexus ratio and how does it affect the IP Box benefit?

Can a non-Cyprus resident own a Cyprus IP Box company?

Is there a minimum substance requirement for the Cyprus IP Box?

How does the Cyprus IP Box compare to the Netherlands innovation box?

Related Guides

Sources

Cyprus Income Tax Law - Article 9B (IP Box provisions). OECD BEPS Action 5 modified nexus approach. Cyprus Tax Department guidance on qualifying IP assets. Updated: April 2026.

Our Cyprus IP Box Calculator lets you model your effective rate based on your qualifying IP income and nexus ratio, and compare it against other EU IP Box regimes including Luxembourg (5.2%), Ireland (6.25%) and the Netherlands (9%).